9.1 – Three Sides To A Coin

You have got a lot of the fundamentals in the past few weeks. This week will introduce you to some of the data that I follow.

Robert Kiyosaki has a saying, “there are three sides to a coin”.

People argue that it’s a good time to buy or bad time to buy. For example “mfh” is overheated or commercial is getting killed by Amazon and e-commerce. I think these are mental justifications by tire kickers not to do anything.

Sophisticated investors live on the edge of the “coin”. They buy deals out our reach of amateurs due to the lack for network/knowledge. These opportunities are undervalued, with undermarket rents, with value add opportunity.

They are patient and don’t stray from standards that make them get crushed in a market correction. (Cashflow from other investments make this possible) They invest following the macro and micro trends and don’t gamble on gimmicks such as guessing where Amazon’s next HQ is going or where the hurricanes just crushed a market.

The trouble is as an outsider is figuring out which of these deals transcends the two side of coin and is on the edge. And starting out it’s going to be slim pickens due to lack of network but you have to push through this rough part.

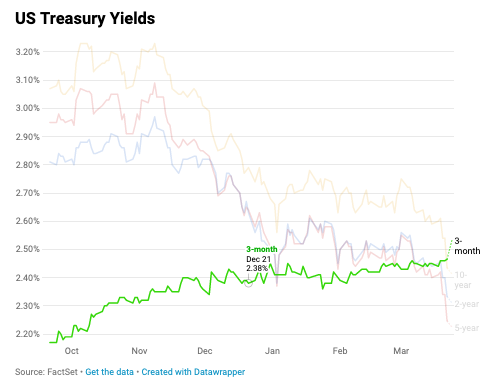

And on March 22. 2019 CNBC announces that the ‘Yield Curve’ inverts as 3-month yield tops 10-year rate.

This is NOT the time to be aggressive in your deal underwriting (lowering reversion cap rates, vacancy rates, and increasing annual rent increases over 2.5%). And its NOT the time to get short term loans (5 years or less).

We have an inverted yield curve which academics call an indicator of a recession…and also the Fed – after raising rates in September and again in December announced it envisions no rate hikes in 2019.

This means that the 3 months yield curve is more attractive than 10 year. This is what we call a “yield curve inversion “.

No regular guy on the street feels this but it impacts the banks greatly. The banks make money by paying retail to CD savings paying ~1% using short term interest rates like 3 months or 2-year yield to the regular guy who walks into the bank for a loan or gives us a 4-5% commercial real estate loan to do a syndication. That arbitrage is how the bank makes money. If short term yield is higher than the 10-year treasury yield, then the banks can’t really make money by arbitrage. The Banks will stop lending. When then banks stop lending, no one can get any loans which leads to a slowdown in economic activities leading to recession. Companies start shipping less and ordering more raw goods and everyone freaks themselves out into being gun shy.

That said it might not be a good time for hotel investing – SimplePassiveCashflow.com/154kira

What I do know that inflation is coming to pay for all this fake money pumped into the system. Those who own a lot of real estate and borrowed 2020 debt are going to win and those sitting on the sidelines will lose.