How the Wealthy Manage Their Money

Walt Disney

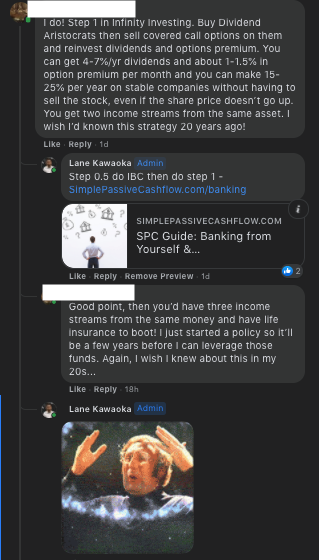

When banks would not initially fund Walt Disney's dream, he became his own bank and borrowed from his own life insurance in order to develop Disney.

Ray Kroc

Ray Kroc was able to pay key employees and McDonald's branding campaign through the liquidity in his whole life insurance policy.