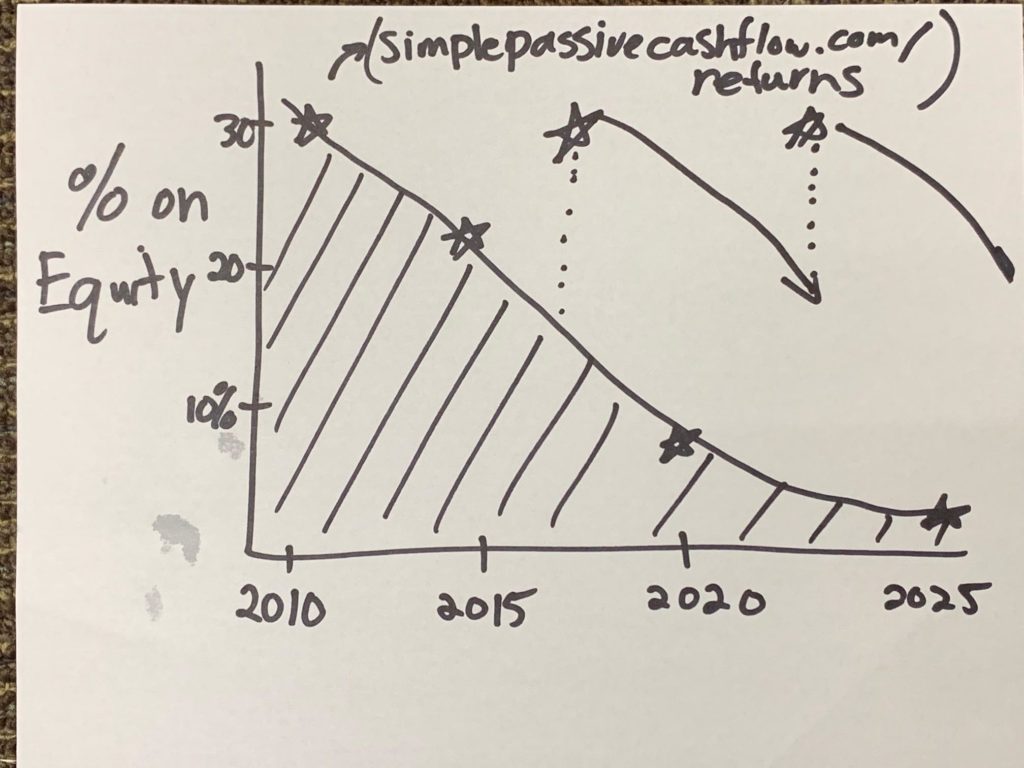

10) Exit Strategy

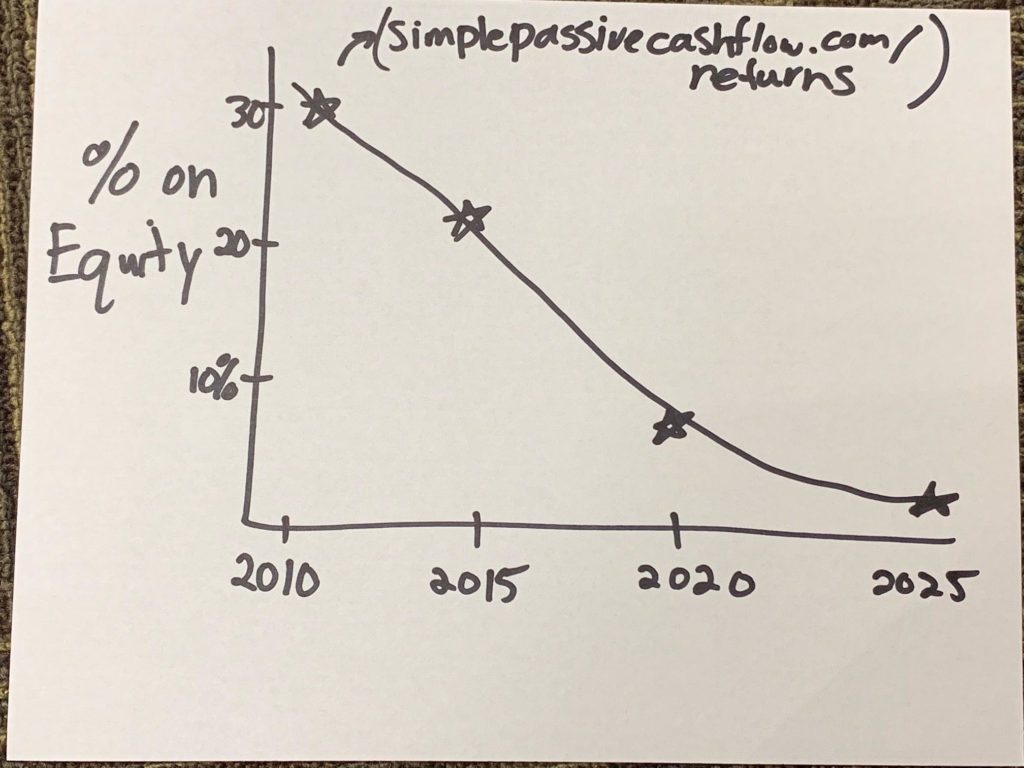

When your property appreciates and your tenant pays down your mortgage your equity position goes up  unfortunately your return on equity goes down.

unfortunately your return on equity goes down.

Tired of investing on your own?

Join us in a larger deal